Online Casino Singapore: Why Unregulated Deposit Gateways Fail Up to Half the Time

Summary: Interviews with operations staff at online gaming platforms describe a consistent consumer risk in Singapore's unregulated payments: unlicensed gateways are far less reliable than the regulated, authorized gateways they imitate. Where a licensed gateway succeeds on nearly every attempt, sources estimate these unofficial channels complete only around 50 to 80 percent of transactions—and beyond the failed payments, some route users through look-alike bank login pages that put their credentials at risk. The figures below are operator estimates shared in interviews, not independently verified statistics.

1. An Unstable Success Rate: Why Unregulated Gateways Fail So Often

Operations staff interviewed for this piece describe a reliability gap rooted in the infrastructure itself. An unregulated gateway is not an official, authorized payment channel; it is an unofficial substitute standing in for one. Sources estimated that these channels complete only about 50 to 80 percent of transactions, meaning that on a bad day as many as half of all deposit attempts can simply fail. No audited data was provided to confirm the range, but every source agreed the success rate is unstable and unpredictable in a way a regulated gateway is not.

The reason is straightforward. A licensed, regulated gateway is built for stability: it has redundant routing, established relationships with banks, uptime obligations, and support teams that keep it running around the clock. An unregulated gateway has none of that. It depends on improvised banking connections that can be closed at any time and patched-together routing with no backup, so when any single link drops, transactions fail. That is why the same payment that would go through instantly on a licensed processor may fail repeatedly here—and why the experience is inconsistent from one attempt to the next.

2. What Payment Methods These Platforms Actually Offer

Our own testing of online casino gaming sites operating in Singapore found a consistent and telling pattern in the deposit options offered. Every platform reviewed relied on some combination of the following:

- Payment gateways (the unofficial, unregulated channels described above)

- Online banking deposits (direct bank transfers, including the look-alike login pages discussed later)

- QR code payments

- Cryptocurrency deposits

What was missing is just as significant as what was present. Across the sites tested, we could not find a single platform offering credit card or PayPal deposits. When our tester attempted a card deposit through the few channels that appeared to accept one, the card-issuing bank blocked the transaction outright.

This absence is a signal in itself. Mainstream, regulated payment methods like credit cards and PayPal come with built-in consumer protections—chargebacks, dispute resolution, and fraud monitoring—and their networks actively block gambling transactions they identify as high-risk or unlicensed. The fact that these platforms fall back on bank transfers, QR codes, and crypto is a direct consequence: they route around the very methods that would give users recourse. For a consumer, the lack of any card or PayPal option is a practical red flag that a platform is operating outside the regulated system.

3. What a Failed Payment Means for the User

When one of these unstable channels drops a transaction, the consequences land on the consumer, not the operator:

- Money in limbo: Sources say a user's payment can be debited from their account or wallet yet never arrive, sitting in a prolonged "pending" state. Because the channel is unlicensed, the depositor typically has no regulator to appeal to and limited prospect of getting the money back.

- Repeated re-tries and overpayment: When a deposit fails, users often try again—and again—raising the chance of a double charge, and leaving them with no clear record or support line to sort it out afterward.

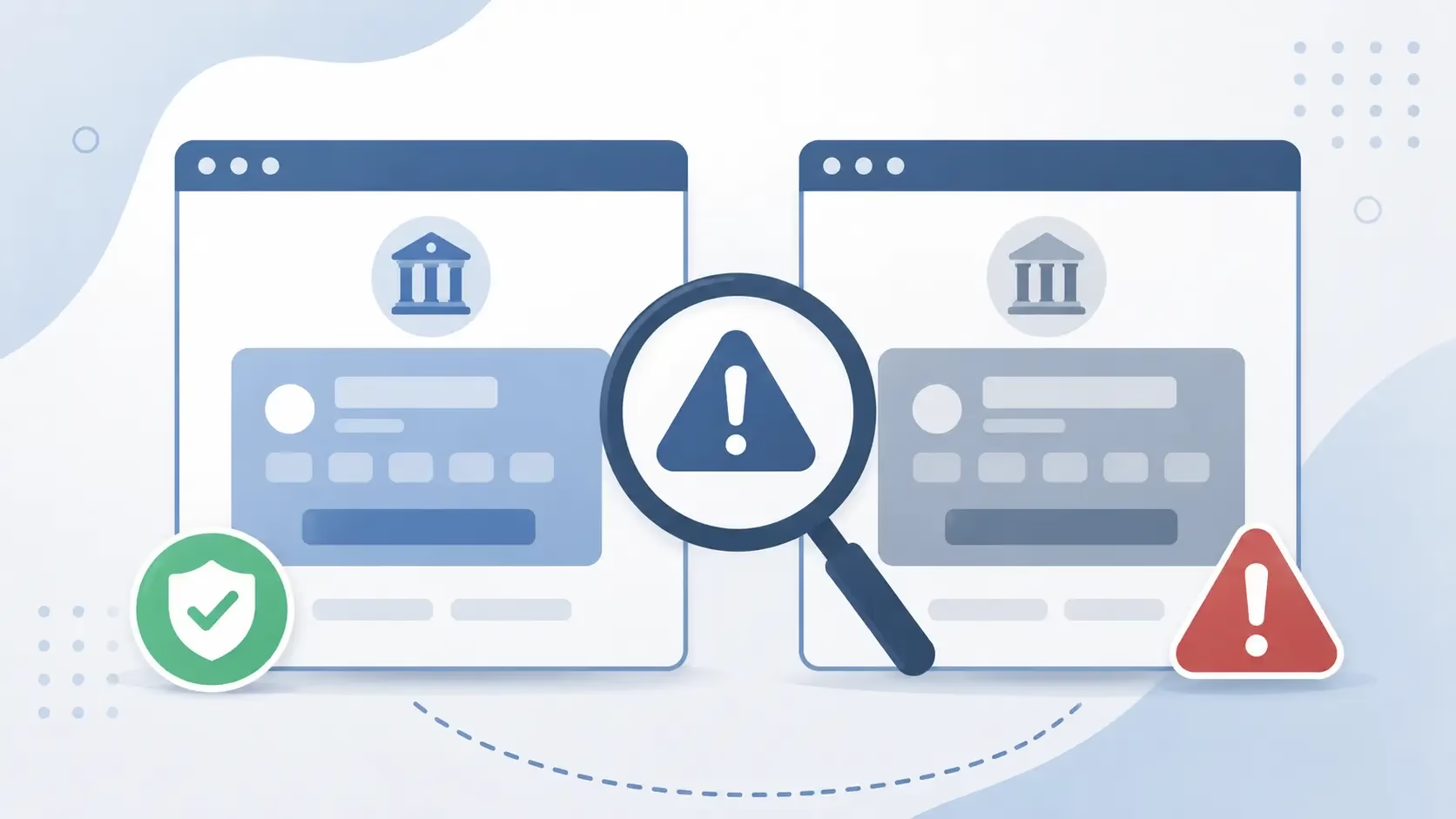

4. Regulated vs. Unregulated Gateways: What Users Should Know

The table below contrasts a licensed, authorized payment gateway with the unlicensed unregulated channels described by sources. The figures are operator estimates, not benchmarked measurements.

| What to compare | Regulated / Authorized Gateway | Unregulated Gateway |

|---|---|---|

| Success rate (estimated) | Consistently high; near every attempt | Unstable, roughly 50–80% |

| If a payment fails | Traceable, with support and dispute options | Funds can be stuck with little recourse |

| Login security | You log in on your bank's own site | May use a cloned, look-alike bank login page |

| Consumer protection | Covered by the licensing regime | None—operates outside regulation |

The takeaway for users is simple: an unlicensed gateway is not just less convenient, it removes the safety net that a regulated one provides.

5. The Bigger Risk: Your Bank Login

Unreliable payments are frustrating, but the more serious danger is what some of these gateways ask users to do. Sources and the broader pattern of these operations indicate that certain unregulated gateways route users through a cloned copy of their bank's login page—an imitation built to look identical to the real thing. A user who types their banking username and password into that page may be handing those credentials directly to whoever controls the gateway, exposing not just the deposit but the entire bank account to theft.

This is the clearest warning sign a user can watch for. A legitimate, regulated payment service never asks you to enter your online-banking username and password on its own or a third-party page—you always log in on your bank's official site or app. If a gaming or payment page asks for your full bank login directly, that alone is reason to stop. The same lack of oversight that makes these channels unreliable is what leaves the door open to credential harvesting.

For consumers, the bottom line is straightforward: money sent through an unlicensed gaming gateway sits outside every consumer-protection safeguard, and the login page you are shown may not be your bank's at all.

Frequently Asked Questions

Methodology & caveats: This consumer-awareness analysis draws on two sources: interviews with internal operations staff at online gaming platforms, and independent hands-on testing of Singapore-facing casino sites by our own tester, including the available deposit methods and an attempted card transaction. The success-rate figures are estimates provided by interview sources and have not been independently audited. Named platforms, gateways, and operational details have been deliberately omitted. The aim is solely to help the public recognize the risks of using unlicensed payment channels—not to guide, endorse, or operate any of them.